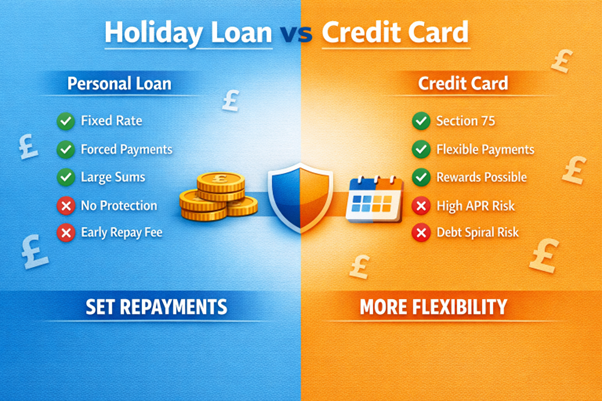

You should have the correct ways of financing your dream vacation. There are two alternatives: a holiday loan and a credit card. The cost of saving or losing hundreds of pounds in the long run rests with the decision between them.

Some travellers rush into high-interest options without realising cheaper alternatives exist just a few clicks away. The three factors that should be considered when selecting your best pick are: the amount of money that you require to borrow, the speed at which you repay the loan, and the form your credit rating takes.

This blog will reveal the actual holiday finance costs in the UK. It will allow you to have fun during your break without having to struggle with the financial hangover the next day.

What is a Holiday Loan?

A personal loan for holiday expenses might bridge the gap when your dream vacation feels just out of reach. These loans let you borrow a set amount upfront and pay it back over time. You can get between £1,000 and £25,000.

Most holiday loans come with fixed interest rates between 3% and 10% if you have decent credit. You'll pay the same amount each month until you clear the debt. The stability helps with budgeting while you're enjoying memories of your time away.

Loan terms are from one to seven years. The long terms mean small monthly payments but more interest overall. Most lenders won't ask you to prove you're using the money for travel. You are free to spend it on flights, hotels, spending money or all three.

- No need to save the full amount before booking

- Fixed payments make budgeting easier after your trip

- Often cheaper than credit cards for larger amounts

- Money arrives in your account before you book

- Application decisions come within 24-48 hours

What is a Credit Card for Holidays?

Credit cards give you a credit limit you can spend up to, then pay back as much as you want each month. The average credit card charges between 22% and 29% APR. This adds up quickly if you only make minimum payments.

The 0% purchase cards don't charge any interest for a set period. It can be from 12 to 21 months. During this time, every penny you pay goes toward clearing your balance, not interest.

Most cards only ask for minimum monthly payments of around 1-3% of your balance. It stretches your debt out for years. Many holiday cards also offer perks like air miles, cashback on spending, or travel insurance.

- Section 75 protection covers purchases between £100-£30,000

- No early repayment fees if you suddenly can pay it off

- Some cards don't charge foreign transaction fees

- Easy to reuse for emergencies during your trip

| Cost Comparison – £3,000 Holiday Debt | |||

| Factor | Holiday Loan (6% APR) | Standard Credit Card (24% APR) | 0% Credit Card |

| Monthly Payment | £159 | £100 | £167 |

| Repayment Term | 24 months | 36+ months | 18 months |

| Total Interest Paid | £189 | £800+ | £0 |

| Total Amount Repaid | £3,189 | £3,800+ | £3,000 |

| Rate Type | Fixed | Variable | Fixed then jumps |

When a Holiday Loan is Cheaper?

The loans often win if you need longer than two years to repay. Their lower interest rates mean substantial savings over standard credit cards for extended payment periods.

Those with average credit scores might not qualify for the best 0% card deals but can still get reasonable loan rates. Loans also create a forced repayment structure.

Holiday loans for bad credit exist for those with troubled financial histories. These products give travel opportunities to people whom credit card companies might reject. They offer predictable payments and can help rebuild your credit score responsibly.

- Forces a clear end date to your holiday debt

- Provides certainty for long-term budget planning

- No risk of rate increases during repayment

- Often more accessible than premium credit cards

When a Credit Card is Cheaper?

Credit cards are the best when you can repay within the 0% period. A 21-month interest-free deal beats any loan if you clear the balance before the promotional period ends.

Section 75 protection gives cards a huge advantage for holiday bookings. You can claim money back from your card provider for purchases between £100 and £30,000 if your travel company goes bust.

If you already have a 0% card with available credit, using it means no new applications or credit checks. Some cards with travel perks can discount your holiday through cashback, air miles or free travel insurance.

- Can be completely interest-free if managed well

- Easy to adjust payments based on monthly finances

- Legal protection if your holiday company fails

- Potential rewards reduce the effective cost further

- No early repayment charges if circumstances change

Cost Comparison

Planning your holiday funding means understanding the true cost of each option.

Holiday Loan Breakdown

Taking out £3,000 at 6% APR over two years means monthly payments of around £159. By the end, you'll have repaid £3,189 total - just £189 in interest. The rate stays the same from day one until your final payment. You'll never face surprise increases.

Standard Credit Card Costs

Putting £3,000 on a regular credit card with 24% APR and making only minimum payments could take over a decade to clear. You'd end up paying more than £2,500 in interest.

0% Credit Card Option

The 0% purchase card charges £3,000 over an 18-month period with no interest. You could pay just £167 monthly and clear it before paying any interest at all. Miss the end date and the rate jumps to 23% or higher overnight. You can expect a 3-5% fee on the amount if you need to transfer the balance later.

Conclusion

The decision between a holiday loan and a credit card does not require any complicated choices. Your vacation should not leave you worrying about finances even after several years. Before booking, you can get time to see the numbers. These ten research minutes would help in saving hundreds of pounds.

The most cost-effective one is always about saving in advance. In case you need to borrow, choose the one that suits your repayment capacity and not necessarily the one that you can easily access. You can write your schedule of repayment prior to your schedule of itinerary.